Financial and digital inclusion ensure everyone, regardless of income or location, can access financial services and digital tools. Together, they empower people, promote economic stability, improve social connection, and create opportunities, while technology and literacy bridge barriers to participation and growth.

In today’s world, access to money and the internet means access to opportunity. But for many people around the world, that access doesn’t exist. Financial and digital inclusion are two major forces helping to close that gap.

They ensure that people, no matter What is Financial and Digital Inclusion? their income or location, can use digital tools and financial services to improve their lives. When both work together, they create a fairer and connected world.

Understanding Financial Inclusion

Financial inclusion is not about handing out free money. It’s about access. Access to tools that let people save, borrow, pay, and protect their finances.

Why Financial Access Matters

When people have a way to safely store their money or take out a small loan, they gain control over their future. They can:

-

Invest in a small business

-

Send their children to school

-

Pay for healthcare or emergencies

-

Avoid loan sharks and unsafe borrowing options

Without financial services, many are stuck using cash only. That means no credit history, no safety net, and limited chances to grow.

Who Gets Excluded Financially?

The financially excluded often live in rural areas or informal communities. Many women, people with disabilities, and those without formal IDs also fall into this category. Their needs are often ignored by traditional banks, leaving them with no secure way to manage money.

What Is Digital Inclusion?

Digital inclusion is more than giving someone internet access. It’s about making sure people can actually benefit from digital tools in their daily lives—financially, socially, and economically.

The Four Pillars of Digital Inclusion

Affordable Access:

Can people afford reliable internet and digital devices?

Digital Skills:

Do they have the knowledge to use smartphones, apps, and online services effectively and safely?

Useful Content:

Is digital content relevant to people’s real needs, available in local languages, and culturally appropriate?

Inclusive Design:

Are websites and apps accessible to everyone, including people with disabilities, low literacy levels, or limited tech experience?

Initiatives like Google Pay in Bangladesh highlight how fintech can accelerate digital inclusion by making digital payments more accessible, encouraging cashless transactions, and bringing more people into the formal financial system—especially when combined with affordable access, digital skills training, and inclusive design.

Without all four pillars in place, the internet risks becoming another barrier instead of a bridge to opportunity.

Digital Exclusion in Daily Life

Think of all the things people do online today — from applying for jobs to video chatting with family. Those who don’t have digital access are missing out on work, education, healthcare, and basic communication.

In many low-income countries, millions still live without reliable internet. Even in wealthier places, many older adults or marginalized groups are offline, simply because they haven’t had the chance to learn.

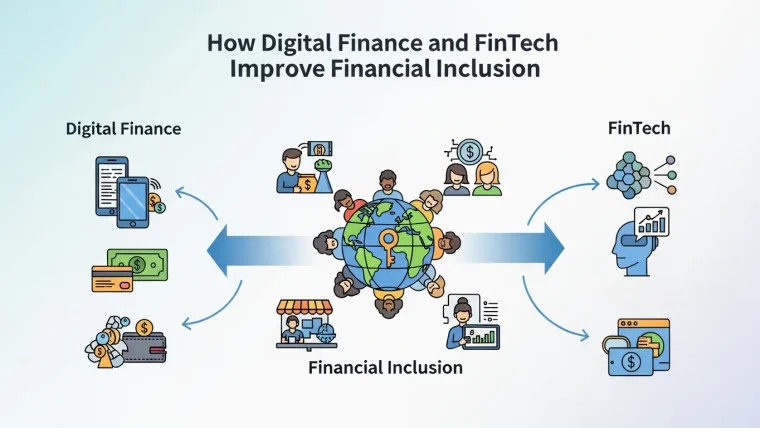

How Financial and Digital Inclusion Work Together

The modern world runs on digital systems. Many financial services today are digital-first or digital-only. That makes digital inclusion a key part of financial inclusion.

Digital Tools for Financial Access

In some countries, digital platforms have replaced traditional banks. Mobile wallets like M-Pesa in Africa or bKash in Bangladesh let users pay bills, send money, and store savings from a simple mobile phone.

These tools are powerful, but they only work if people can use the technology. So, without digital skills or access, financial inclusion is nearly impossible.

A Two-Way Relationship

It goes both ways. If someone can’t access financial services, they may have no reason to be online. But once they’re included financially, digital tools become useful—for tracking spending, shopping online, or getting paid digitally.

The Role of Technology in Financial and Digital Inclusion

Technology acts as the bridge that connects financial and digital inclusion. Without the right technology, access alone is not enough to create real impact.

Key technologies driving inclusion include:

-

Mobile phones enabling banking without physical branches

-

Cloud-Based Platforms reducing service costs

-

Digital IDs simplifying account verification

-

Fintech apps designed for low literacy users

When technology is affordable and user-friendly, it removes barriers that once kept millions outside the financial system.

Real-Life Examples of Inclusion

Kenya: M-Pesa and Mobile Banking

M-Pesa turned phones into banks in rural Africa. People could finally send and receive money without traveling hours to a physical bank. This digital solution became a financial revolution.

India: Aadhaar-Linked Financial Services

India linked national ID cards to bank accounts and digital wallets. This helped millions of people access government benefits directly into their accounts. It connected financial and digital systems in a smart, scalable way.

Latin America: Fintech for the Unbanked

In countries like Brazil and Mexico, fintech startups have built mobile apps that work with limited data, low-end phones, and in local languages—bringing people into the financial system one screen at a time.

Challenges to Financial and Digital Inclusion

While progress has been made, many barriers still remain.

Common Barriers People Face

-

Lack of infrastructure: No signal, no broadband

-

Cost: Devices and data are still expensive for low-income groups

-

Low trust: Some communities distrust banks or digital platforms

-

Limited literacy: Reading and tech skills are still major hurdles

-

Cultural resistance: Gender roles or social norms can prevent access

Each of these factors can shut someone out of financial and digital systems—especially if they face more than one challenge at once.

The Importance of Financial and Digital Literacy

Access alone is not enough. Without the knowledge to use financial and digital tools properly, people can still face exclusion, mistakes, or exploitation. Financial and digital literacy bridge this gap by enabling individuals to engage with technology and financial systems safely, confidently, and independently.

These forms of literacy equip people with essential life skills, such as understanding how savings, loans, interest, and digital payment systems work. They also help individuals learn how to protect their personal and financial information, reducing the risk of data breaches, identity theft, and financial fraud.

In an increasingly digital world, knowing how to use smartphones, apps, and online platforms effectively is critical. Digital literacy allows people to access services, communicate, and manage finances with ease, while financial literacy helps them evaluate options, plan for the future, and avoid unnecessary debt.

Equally important is the ability to identify fraud, scams, and misinformation. With rising online threats, literacy empowers users to recognize warning signs, verify information, and make informed decisions.

Ultimately, financial and digital literacy transform access into true empowerment. They ensure that individuals are not just users of systems, but confident decision-makers who can navigate opportunities responsibly and build long-term security.

Economic Stability

Financial and digital inclusion help people withstand shocks. Whether it’s a job loss or a medical emergency, access to money and tools helps people bounce back faster.

Social Connection

Being digitally connected means more than convenience. It allows people to stay in touch, learn new skills, and participate in their communities—even when physical distance keeps them apart.

Empowering the Marginalized

Inclusion is especially important for women, the elderly, people with disabilities, and refugees. These groups often face the most exclusion but benefit the most from tailored access.

Financial and Digital Inclusion for Women and Marginalized Groups

Women and marginalized communities face unique challenges that require targeted inclusion strategies.

Key inclusion benefits for these groups:

-

Greater financial independence for women

-

Safer access to money without intermediaries

-

Improved access to education and healthcare services

-

Stronger participation in local and digital economies

Inclusive design ensures that systems work for everyone—not just the most privileged users. Keep reading AI and Machine Learning

How Businesses Benefit from Financial and Digital Inclusion

Financial and digital inclusion is not only a social good—it also creates economic value for businesses and institutions.

Business-level advantages include:

-

Access to untapped markets and new customers

-

Lower transaction and service delivery costs

-

Increased customer loyalty and trust

-

Better data insights for product innovation

Inclusive systems grow economies while strengthening long-term business sustainability

What’s Being Done to Improve Inclusion?

Government Actions

Some governments are building low-cost internet networks in rural areas or subsidizing smartphones for poor families. Others are offering digital ID systems that simplify banking access.

Private Sector Innovation

Tech companies and startups are designing services for people who have never used a bank or logged onto the internet before. These innovations are making inclusion more realistic, one user at a time.

Community Involvement

Local programs that train people in digital and financial literacy are helping to bridge the gap. When communities lead the charge, solutions are more trusted and effective.

The Future of Financial and Digital Inclusion

The future of financial and digital inclusion will be shaped by smarter technology and human-centered design.

Key trends shaping the future:

-

AI-driven credit scoring for people without credit history

-

Offline-friendly apps for low-connectivity regions

-

Voice-based interfaces for low-literacy users

-

Integration of digital inclusion with healthcare and education

Inclusion will move beyond access and focus more on usability, dignity, and long-term impact.

Financial and Digital Inclusion at a Glance

| Aspect | Financial Inclusion | Digital Inclusion |

|---|---|---|

| Core Focus | Access to financial services | Access to digital tools & skills |

| Key Tools | Bank accounts, mobile wallets, credit | Internet, devices, digital platforms |

| Main Benefit | Financial security & opportunity | Information, connection & services |

| Major Barrier | Lack of formal banking access | Cost, skills, accessibility |

| Shared Goal | Economic empowerment | Social and economic participation |

Conclusion

Financial and digital inclusion is more than access—it’s empowerment. By combining accessible financial services with digital tools, people can manage finances securely, participate in the digital economy, and improve their quality of life. Inclusion is a long-term process that requires technology, literacy, and human-centered design. As more individuals gain access, societies and businesses benefit through stronger economies, innovation, and social cohesion. Step by step, with the right approach, inclusion can create a fairer, more connected world for everyone.

FAQs on Financial and Digital Inclusion

1. What is financial and digital inclusion?

Financial inclusion ensures access to banking, credit, and payment systems. Digital inclusion ensures people can access and effectively use digital tools and the internet. Together, they empower people to participate fully in society and improve economic and social opportunities.

2. Why is financial inclusion important?

Financial inclusion allows people to:

-

Save money safely

-

Borrow responsibly

-

Access credit and financial services

-

Avoid unsafe borrowing practices

It ultimately improves economic stability and creates opportunities for growth.

3. Why is digital inclusion important?

Digital inclusion connects people to essential resources. Without access to the internet, devices, or digital skills, individuals cannot fully benefit from:

-

Online services

-

Education and learning platforms

-

Economic opportunities

-

Communication and social connection

4. Who is typically excluded from financial and digital services?

The following groups often face exclusion:

-

Rural populations and informal communities

-

Low-income families

-

Women and marginalized groups

-

Elderly people

-

People with disabilities

-

Those without formal IDs or documentation

5. What are the main barriers to inclusion?

Common challenges include:

-

Lack of infrastructure: Limited internet, mobile connectivity, or bank branches

-

High costs: Expensive devices, data, or banking fees

-

Low trust: Distrust in banks or digital platforms

-

Limited literacy: Low financial or digital literacy

-

Cultural resistance: Social norms or gender restrictions

6. How do financial and digital inclusion work together?

Financial services increasingly rely on digital platforms, such as mobile wallets, online banking, and fintech apps. Digital access allows people to use financial tools efficiently, creating a mutually reinforcing cycle where inclusion in one area promotes inclusion in the other.

7. What role does technology play in inclusion?

Technology acts as the bridge between people and services. Key tools include:

-

Mobile phones enabling banking without physical branches

-

Cloud-based platforms reducing service costs

-

Digital IDs simplifying account verification

-

Fintech apps designed for low-literacy or low-connectivity users

8. How can literacy improve inclusion?

Financial and digital literacy empowers individuals to:

-

Understand basic savings, loans, and payments

-

Protect personal and financial data

-

Navigate smartphones, apps, and online platforms safely

-

Identify fraud and misinformation

Literacy transforms access into real empowerment.

9. How do governments promote inclusion?

Governments support inclusion through:

-

Building low-cost internet networks in rural areas

-

Subsidizing smartphones or devices for low-income families

-

Implementing digital ID systems for easier banking access

-

Providing financial and digital literacy programs

10. How can businesses benefit from inclusion?

Financial and digital inclusion also creates economic value for businesses:

-

Access to untapped markets and new customers

-

Lower transaction and service delivery costs

-

Increased customer loyalty and trust

-

Better data insights for innovation and product development

11. What are some real-world examples of inclusion?

-

Kenya: M-Pesa mobile banking revolutionized financial access in rural areas

-

India: Aadhaar-linked financial accounts connected millions to digital banking and government services

-

Latin America: Fintech apps designed for low-income populations improved financial access via low-data mobile solutions

12. What is the future of financial and digital inclusion?

The future will focus on technology and human-centered solutions:

-

AI-driven credit scoring for people without traditional credit histories

-

Offline-friendly apps for low-connectivity regions

-

Voice-based interfaces for low-literacy users

ecommerce growth strategy : Transforming Education Through Calm and Focus

What Is Financial Technology (FinTech)? Everything You Need to Know

Digital Twin Technology in Finance: How Virtual Models Are Transforming Risk Management

AI Credit Scoring: Revolutionizing SME Banking and Digital Loans

ecommerce growth strategy : Transforming Education Through Calm and Focus

business exit strategy : Transforming Education Through Calm and Focus

The True Meaning of Digital Transformation Consulting in Education

Sustainable Digital Finance: Green Investing Strategies